You’ve done your research, and you’re ready to purchase a home. Your credit report hits the mark, so now you’re ready to start checking out mortgage loan options. This loan can take years to pay off, so it’s a good idea to shop around to pick the best option for you.

Credit scores play a large role in the cost of a mortgage. If the score is lower, it may contribute to higher interest rates and a higher monthly mortgage payment.

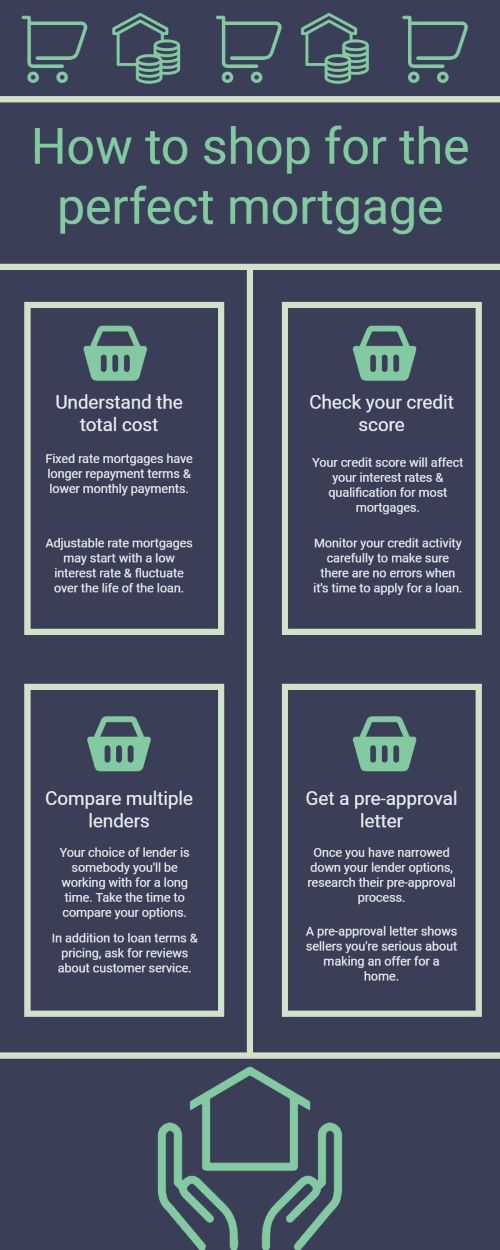

A fixed rate mortgage is a great option if you don’t want the interest rate to alter with time. This type of loan has a preset rate, which is typically paid over the span of 15 or 30 years. Longer loan terms will decrease your monthly payment. Over the lifespan of this loan, the interest rate will remain constant.

Adjustable rate mortgages may start with a fixed interest rate, but are subject to change. This means if the insurance and property tax increase over time, you may see this included in the mortgage payment. Mortgages are made up of your property tax, principal, insurance and interest rates. Changes to any of these factors can affect your monthly payment.

Your credit score will help a mortgage lender determine if you’re qualified to take on the loan and can handle the interest rates involved. You want to stay on top of checking your credit history to make sure the score is where it should be. A history of paying your bills on time will work in your favor.

There are so many options available - it isn’t enough to just know the monthly payment. Finding the right fit for a mortgage lender can be a tricky process.

Consult your real estate agent for suggestions. They often have experience with multiple lenders, so they can help you create a list of firms fitting your criteria. This will provide the opportunity to compare interest rates, monthly payments and figure out which option is best for you.

Once you have narrowed down your lender prospects, research their pre-approval letter process. Make sure your credit score is acceptable and then request an approval letter. A pre-approval letter is not an official offer for a loan, but signifies a lender has inquired about your financial state and affirmed you meet requirements to be offered funding. Having a pre-approval letter also shows sellers you’re serious about putting in a valid offer for their property.

When you’re ready to buy a house, check and compare quotes and negotiate loan rates. Make sure your credit score is at a place accepted by most lenders. Once you have found a potential lender, you’ll be well on your way to homeownership.

As a military spouse for over 17 years, I understand the challenges of moving and relocating. I have lived in Eastern North Carolina for over three years and am familiar with the area. As a homeowner and business owner, I understand the importance of making one of the largest asset investments you will make. My goal is to build a long-lasting relationship with you throughout the home buying or selling process and I am 100% committed to providing you with the highest level of personal service. Whether you are buying, selling, investing, or just curious about the local market, I would love to offer my support and services.